Skip to:

Skip to:

NEW EUROPEAN RULES ON THE DEFINITION OF DEFAULT: UNDERSTANDING HOW TO DEAL WITH THE CHANGES

As of 1 January 2021, UniCredit will apply the new European rules on the classification of defaulting counterparties (better known as "defaults").

The new regulation establishes more restrictive criteria and methods for the classification of default compared to those adopted by Italian intermediaries until now, with the aim of harmonising approaches to defining default and identifying the conditions of unlikeliness to pay across financial institutions and the different jurisdictions of EU member states.

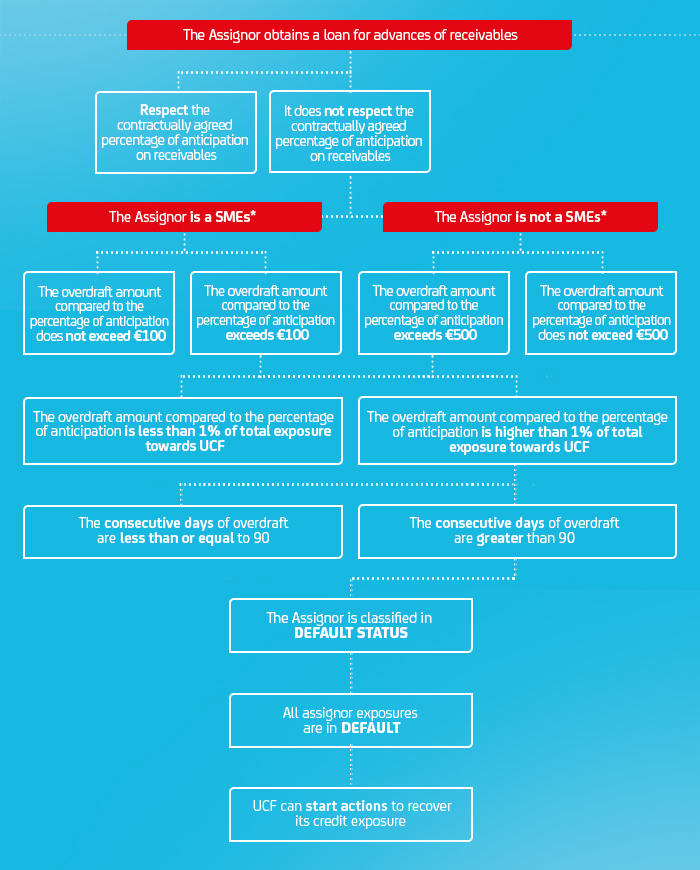

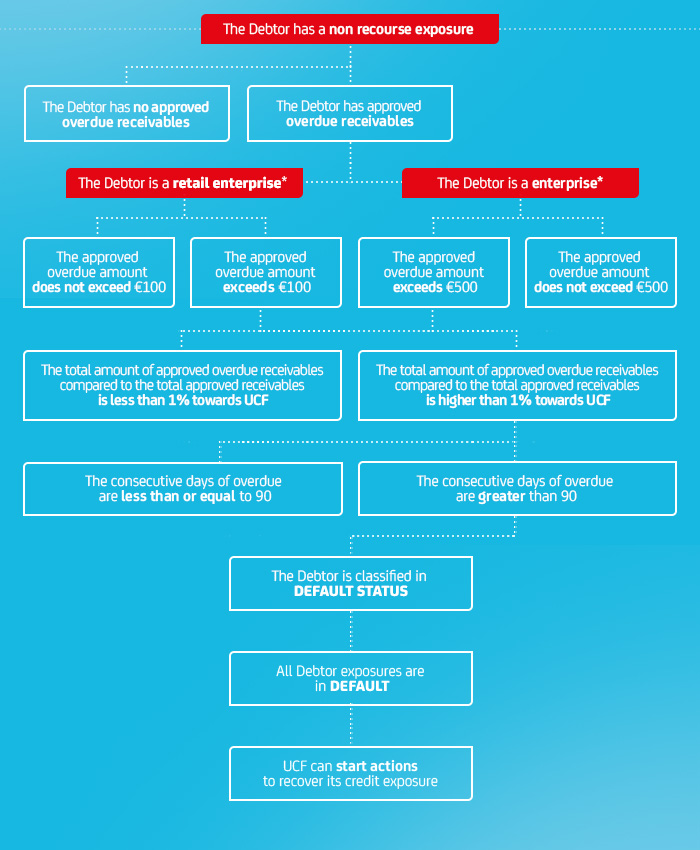

The main changes envisage banks automatically defining customers as defaulting where there are arrears for over 90 days, for an amount which is, at the same time:

above €100 and above 1% of the Banking Group's total exposure

Small and Medium Enterprises (SME): business owners, freelancers, sole traders and businesses with turnover of less than 5 million Euros and exposure to the bank of less than 1 million Euros

above €500 and above 1% of the Banking Group's total exposure

The calculation takes into account positions in place across all UniCredit Group companies.

There are also other changes, including:

- the definition of credit obligations indicated as Unlikely to pay

- the spread of the default

- the minimum period of permanence of the default status

- the assessments that the company must carry out to reclassify the customer's status as non-defaulting

Once the arrears have been cleared, and at least 90 days have elapsed from that time without further arrears situations or prejudicial events occurring, the default reporting obligation will lapse.

ASSIGNMENT OF ADVANCES WITH RECOURSE AND NON-RECOURSE

(Formal non-recourse means without recourse with risk mitigation clauses)

DEBTOR ASSIGNED AS NON-RECOURSE

Effective non-recourse means non-recourse without risk mitigation clauses and outright purchases (with IFRS compliant derecognition). Exposure means a debt against an approved non-recourse or purchased outright receivable.

IT IS IMPORTANT TO FOLLOW THE NEW DEFAULT RULES

It is therefore essential for assignors to respect the contractually established part of the advance for receivables and for debtors to promptly meet all payment deadlines set out in the contract and to comply with the repayment plan for debts, ensuring that even small amounts are not neglected, to avoid a default classification that will entail a reporting obligation to the Bank of Italy's Central Risk Bureau.

Here are the answers to the most frequently asked questions (FAQ) about the new Default rules.

Regulatory references

EBA/GL/2016/07 “Guidelines on the application of the definition of default under Article 178 of Regulation. (EU) No 575/2013

EBA/RTS/2016/06 “New Technical Standards on the materiality threshold for credit obligations past due” integrating the EU Delegated Regulation No. 171/2018 of the European Commission of 19 October 2017